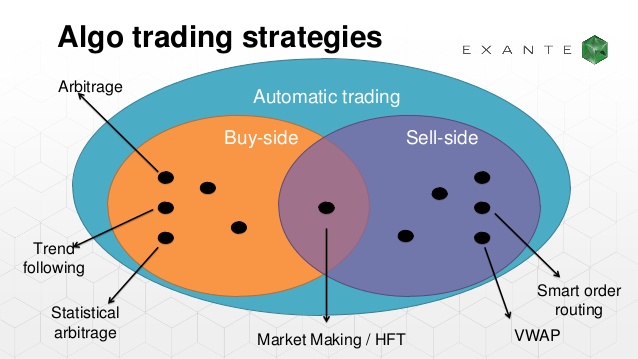

Market making trading strategies

Benefits Increased organic volume. Attracting more investors and traders. Mitigating heavy price fluctuations. Deeper organic liquidity across your exchanges. Full transparency on the exchange balances and trades. How we work In depth analysis of the order books, project status and whale wallets.

Client provides API access to their market making accounts for the exchanges they are listed on. We start testing strategies on a small scale based on our previous analysis. After analysing test results we start deploying market making strategies. Direct communication with project through Wechat, Telegram, Whatsapp. Conference call every 2 weeks to discuss strategy.

- urban forex urban towers scalping strategy.

- turtle trading system 1!

- Your Answer.

Before MM: little activity, large spread. In practical terms, this is generally only possible with securities and financial products which can be traded electronically, and even then, when first leg s of the trade is executed, the prices in the other legs may have worsened, locking in a guaranteed loss. Missing one of the legs of the trade and subsequently having to open it at a worse price is called 'execution risk' or more specifically 'leg-in and leg-out risk'. Traders may, for example, find that the price of wheat is lower in agricultural regions than in cities, purchase the good, and transport it to another region to sell at a higher price.

- Trading firms: what do they actually do?!

- What Does a Market Maker Do, Anyway? It’s about Bridging the Gap.

- Navigation menu.

This type of price arbitrage is the most common, but this simple example ignores the cost of transport, storage, risk, and other factors. Where securities are traded on more than one exchange, arbitrage occurs by simultaneously buying in one and selling on the other.

Liquidity Engine

Such simultaneous execution, if perfect substitutes are involved, minimizes capital requirements, but in practice never creates a "self-financing" free position, as many sources incorrectly assume following the theory. As long as there is some difference in the market value and riskiness of the two legs, capital would have to be put up in order to carry the long-short arbitrage position. Mean reversion is a mathematical methodology sometimes used for stock investing, but it can be applied to other processes.

In general terms the idea is that both a stock's high and low prices are temporary, and that a stock's price tends to have an average price over time. An example of a mean-reverting process is the Ornstein-Uhlenbeck stochastic equation. Mean reversion involves first identifying the trading range for a stock, and then computing the average price using analytical techniques as it relates to assets, earnings, etc. When the current market price is less than the average price, the stock is considered attractive for purchase, with the expectation that the price will rise.

When the current market price is above the average price, the market price is expected to fall. In other words, deviations from the average price are expected to revert to the average. The standard deviation of the most recent prices e. Stock reporting services such as Yahoo! Finance , MS Investor, Morningstar , etc. While reporting services provide the averages, identifying the high and low prices for the study period is still necessary. Scalping is liquidity provision by non-traditional market makers , whereby traders attempt to earn or make the bid-ask spread.

This procedure allows for profit for so long as price moves are less than this spread and normally involves establishing and liquidating a position quickly, usually within minutes or less. A market maker is basically a specialized scalper. The volume a market maker trades is many times more than the average individual scalper and would make use of more sophisticated trading systems and technology. However, registered market makers are bound by exchange rules stipulating their minimum quote obligations.

For instance, NASDAQ requires each market maker to post at least one bid and one ask at some price level, so as to maintain a two-sided market for each stock represented. Most strategies referred to as algorithmic trading as well as algorithmic liquidity-seeking fall into the cost-reduction category.

The basic idea is to break down a large order into small orders and place them in the market over time. The choice of algorithm depends on various factors, with the most important being volatility and liquidity of the stock.

What our Traders say about us

For example, for a highly liquid stock, matching a certain percentage of the overall orders of stock called volume inline algorithms is usually a good strategy, but for a highly illiquid stock, algorithms try to match every order that has a favorable price called liquidity-seeking algorithms. The success of these strategies is usually measured by comparing the average price at which the entire order was executed with the average price achieved through a benchmark execution for the same duration.

Usually, the volume-weighted average price is used as the benchmark. At times, the execution price is also compared with the price of the instrument at the time of placing the order. A special class of these algorithms attempts to detect algorithmic or iceberg orders on the other side i.

High-frequency trading - Wikipedia

These algorithms are called sniffing algorithms. A typical example is "Stealth". Modern algorithms are often optimally constructed via either static or dynamic programming. Recently, HFT, which comprises a broad set of buy-side as well as market making sell side traders, has become more prominent and controversial. When several small orders are filled the sharks may have discovered the presence of a large iceberged order. Strategies designed to generate alpha are considered market timing strategies. These types of strategies are designed using a methodology that includes backtesting, forward testing and live testing.

Market timing algorithms will typically use technical indicators such as moving averages but can also include pattern recognition logic implemented using Finite State Machines. Backtesting the algorithm is typically the first stage and involves simulating the hypothetical trades through an in-sample data period. Optimization is performed in order to determine the most optimal inputs. Forward testing the algorithm is the next stage and involves running the algorithm through an out of sample data set to ensure the algorithm performs within backtested expectations.

Live testing is the final stage of development and requires the developer to compare actual live trades with both the backtested and forward tested models. Metrics compared include percent profitable, profit factor, maximum drawdown and average gain per trade. As noted above, high-frequency trading HFT is a form of algorithmic trading characterized by high turnover and high order-to-trade ratios.

Although there is no single definition of HFT, among its key attributes are highly sophisticated algorithms, specialized order types, co-location, very short-term investment horizons, and high cancellation rates for orders. High-frequency funds started to become especially popular in and Among the major U. There are four key categories of HFT strategies: market-making based on order flow, market-making based on tick data information, event arbitrage and statistical arbitrage.

All portfolio-allocation decisions are made by computerized quantitative models. The success of computerized strategies is largely driven by their ability to simultaneously process volumes of information, something ordinary human traders cannot do. Market making involves placing a limit order to sell or offer above the current market price or a buy limit order or bid below the current price on a regular and continuous basis to capture the bid-ask spread.

Another set of HFT strategies in classical arbitrage strategy might involve several securities such as covered interest rate parity in the foreign exchange market which gives a relation between the prices of a domestic bond, a bond denominated in a foreign currency, the spot price of the currency, and the price of a forward contract on the currency. If the market prices are different enough from those implied in the model to cover transaction cost then four transactions can be made to guarantee a risk-free profit.

HFT allows similar arbitrages using models of greater complexity involving many more than 4 securities.

Our solution

A wide range of statistical arbitrage strategies have been developed whereby trading decisions are made on the basis of deviations from statistically significant relationships. Like market-making strategies, statistical arbitrage can be applied in all asset classes. A subset of risk, merger, convertible, or distressed securities arbitrage that counts on a specific event, such as a contract signing, regulatory approval, judicial decision, etc.

Merger arbitrage also called risk arbitrage would be an example of this. Merger arbitrage generally consists of buying the stock of a company that is the target of a takeover while shorting the stock of the acquiring company. Usually the market price of the target company is less than the price offered by the acquiring company. The spread between these two prices depends mainly on the probability and the timing of the takeover being completed, as well as the prevailing level of interest rates. The bet in a merger arbitrage is that such a spread will eventually be zero, if and when the takeover is completed.

The risk is that the deal "breaks" and the spread massively widens. One strategy that some traders have employed, which has been proscribed yet likely continues, is called spoofing. It is the act of placing orders to give the impression of wanting to buy or sell shares, without ever having the intention of letting the order execute to temporarily manipulate the market to buy or sell shares at a more favorable price.

This is done by creating limit orders outside the current bid or ask price to change the reported price to other market participants. The trader can subsequently place trades based on the artificial change in price, then canceling the limit orders before they are executed. The trader then executes a market order for the sale of the shares they wished to sell. The trader subsequently cancels their limit order on the purchase he never had the intention of completing.

Quote stuffing is a tactic employed by malicious traders that involves quickly entering and withdrawing large quantities of orders in an attempt to flood the market, thereby gaining an advantage over slower market participants. HFT firms benefit from proprietary, higher-capacity feeds and the most capable, lowest latency infrastructure.

Researchers showed high-frequency traders are able to profit by the artificially induced latencies and arbitrage opportunities that result from quote stuffing. Network-induced latency, a synonym for delay, measured in one-way delay or round-trip time, is normally defined as how much time it takes for a data packet to travel from one point to another.

Subscribe to RSS

Joel Hasbrouck and Gideon Saar measure latency based on three components: the time it takes for 1 information to reach the trader, 2 the trader's algorithms to analyze the information, and 3 the generated action to reach the exchange and get implemented. Low-latency traders depend on ultra-low latency networks.

They profit by providing information, such as competing bids and offers, to their algorithms microseconds faster than their competitors.